How should new risk (COVID19) inform investment decisions?

Should our policies and processes be reviewed/ challenged or should we depend on them more than ever?

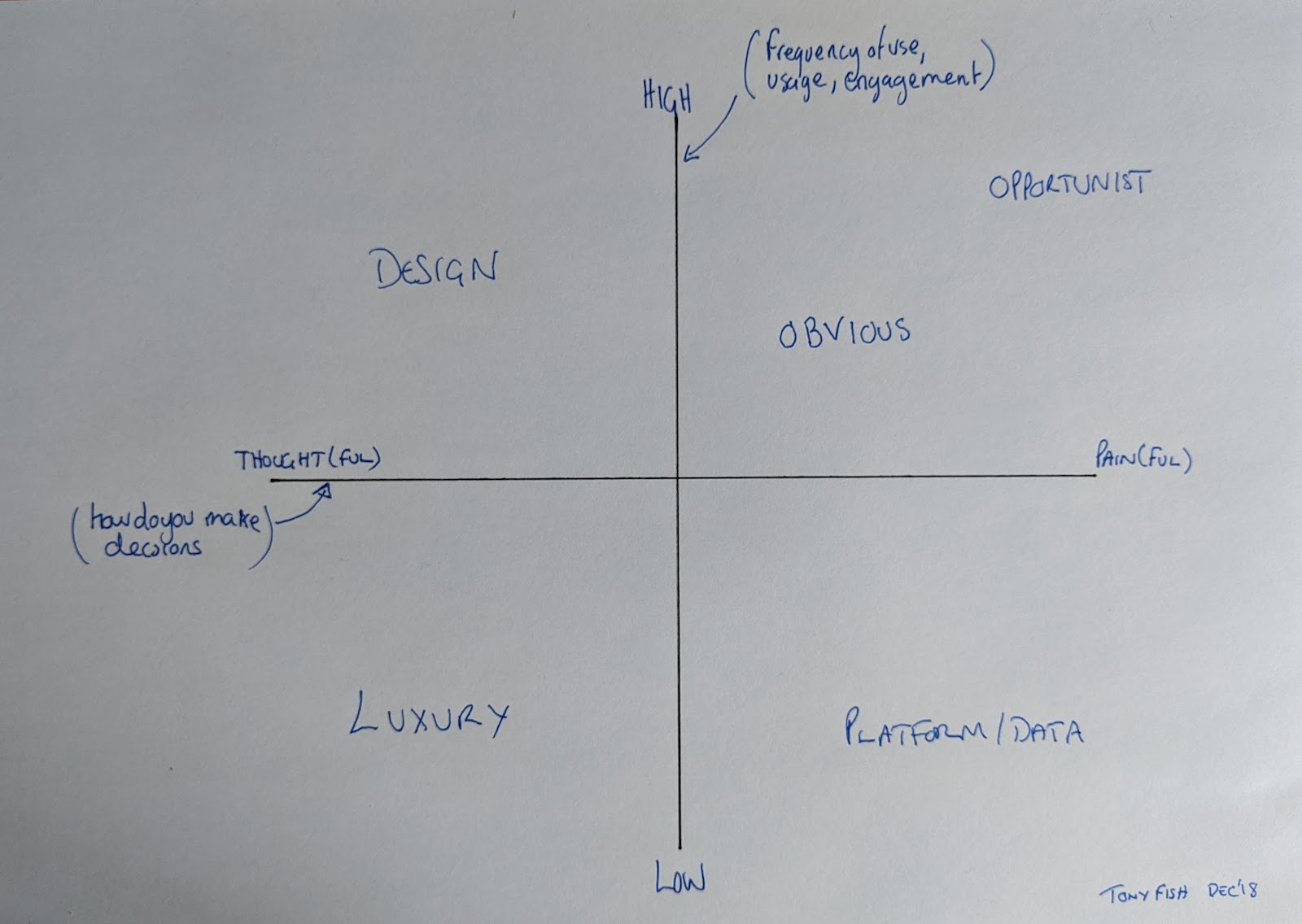

This short article walks through a framework to support complex investment decisions, especially during turbulent times. It is possible to make excellent returns (on investment) in all quadrants, don’t be fooled into thinking that one quadrant is the best (or better). Each quadrant has unique characteristics; the flow is to go through each one in turn, starting top right. However, before that it is worth examining the axes.

The horizontal axis (X) is “how a decision is made”

The extremes of the X-axis extends are Thought(ful) and Pain(ful). A thought(ful) decision means a) you are making an investment decision based on your experience and gut instinct, there is deep analysis and the key is that you have time to consider the options and consequences. b) The purchase decision (demand) for products and service at this extreme is slow and considered. You have time and there is no immediacy of action from pain.

The opposite end of the X-axis is pain(ful). At this extreme you are a) solving a current, tangible and real problem whilst having a large amount of pain attached to it. The investment case is market driven. b) The purchase decision is that it solves the pain right now. Taking away pain is a core driver. In either case pain is not qualified, but take it to be literal and economic (wanted, demanded, reduce cost, new customers, advantage). Unlike thoughtful decisions which have time, pain is driven by urgency.

The vertical axis (Y) is “frequency of engagement”

The Y-axis is all about how often a product or service will be used, from low to high. Used in this case means frequency of use, the actual usage, how often used, engagement or experience depending on the product of service. High engagement/ usage implies every minute, every hour, every day. Low or infrequent engagement is tending towards monthly, annually or even once or twice in a lifetime. There is no specific scale, it is a judgement.

The quadrants

1. OBVIOUS. Top Right. Such is our bias and preference for this quadrant we are automatically prepositioned to think it is the best quadrant. However this quadrant is probably the riskiest. Yes the solution is focussed on solving high-pain problems with massive usage and engagement; but everyone has done the same analysis! Competition comes here really fast and drives price down quickly. Growth is epic, branding is enthralling and users are quickly confused with choice. With many players entering a market, many backed with significant investment for disruption; it becomes very messy very quickly and that kills exits and returns apart from the first to exit who should do extremely well. Later players are mopped up often at a discount to the market by a “strategic investor” exercising a preference or a final roll up where the returns are paper thin.

Two exceptions which make this segment always super interesting:

- non-compliant thinking. This is where the team is able to bring a tectonic shift in the economics and or costs often using adjustment market thinking and technology. The team has discovered a way of creating something new, or delivering the same, or better with a totally different cost base. PayPal (no regulation), EBAY (no logistics), AirBnB (no assets), UBER (no cars), Facebook (user generated content), Amazon (no retail cost). These are gems but difficult to find.

- Inside Advantage this is where a team operating in a market knows something that is only known to existing operators, an insider's advantage. Such insight may lead to new IP, patents or processes. They may have access to a unique channel, have existing customers who want something new, partnerships or something else that provides a defendable and definable long term economic benefit. Again gems but difficult to sort the Cubic Zirconia from Diamonds

Note: Opportunistic. There are opportunities that emerge because of a significant shift/ change. Opportunistic teams can respond and modify a pitch to match language and demand. Great care has to be applied to the analysis to unpick if this is just a short term spike or an investment theme. Not all that glitters is gold.

Note: First mover, something utterly unique and brand new is Design; where we will go next in terms of quadrants.

Note: Solutions that solve pain(ful) may not mean the user knows about it/ recognises it. It is very easy to get duped into thinking that education and marketing are not critical for success, or it is obvious.

2. DESIGN. Top left. Super high engagement but is not really solving a problem that is painful, think iPhone. Nokia has the best UX. Phone made phone calls and we really did not demand a smartphone. We did not need a camera, we did not need apps and we did not need to spend a significant proportion of disposable income on a new bit of unproven tech. But man it is beautiful. The battery was poor, the UX was poor, it could not really make a phone call and it was expensive. Design has a bunch of unique features and characteristics that make it very good for investment, but poor design of the model, high dependency, lack of control and poor ecosystems (betamax) even with excellence technology does not deliver returns. Design is not about technology and there is never sufficient data to provide assurance.

3. LUXURY. Bottom left. You have to overcome that bias even to read about this quadrant being able to be positive. However luxury is a beautiful segment and can delivery better returns than top right. Luxury does not solve a pain and you tend to think about and want the products/ services in this space. Usage is infrequent, whilst you may wear Prada shoes every day, they are probably different ones. Luxury has a unique set of barriers to entry associated with price, demand, quality and branding. It is based on understanding users and behavioural economics as well as manipulation. Successful investments here can deliver 100 times return but the risks and volume of investments make this a difficult separate good from anything else. Data will always be too late to prove this market, this is based on complex judgment, experience and gut feel.

4. PLATFORM AND DATA. Bottom Right. Back 20 years ago this quadrant was an empty space but now due to connectivity and digital services this quadrant is of significant focus. Think scale and the long tail. How to serve 100 million customers moment by moment with a unique service for every person (personalisation), all on one platform. The data is the driver. The ability here is not solving the same pain problem for every customer (top right) but solving each and every unique customer problem. You are joined by other customers who have the same pain, but there may only be 10 right now, and you may not come back for 5 years. Data and platforms can serve the long tail of niches. Everything is now data so the issue in this quadrant as it is maturing is seeking non-compliant thinking.

The purpose here was to say that investment is still going to make a lot of sense, and in each quadrant good returns can be made for venture/ risk money. In reality the thesis has not changed.

When thinking about a market in any quadrant investors will consider

How do the actors in the market act for their own self interest and what does it mean?

Does the market only have pull as the players gain benefit, who funds demand generation?

Consensus of need is not sufficient to justify a market at scale

Does this have non-systems level dependency for success or are there single or few controllers that you can influence